What Happens Next? EFRAG’s Post-Consultation Roadmap for the VSME Standard

What Happens Next? EFRAG’s Post-Consultation Roadmap for the VSME Standard

On June 3, 2026, the European Commission officially closed its public consultation on the draft Voluntary Sustainability Reporting Standard for Non-Listed SMEs (VSME). This consultation represents one of the most critical steps in EFRAG's mission to standardize supply chain ESG disclosures across the European Union.

For months, small and medium-sized enterprises (SMEs), corporate buyers, digital service providers, and accounting associations have submitted technical feedback to refine the framework.

Now that the public feedback period has ended, what happens next? What is standard-setter EFRAG's roadmap to finalize the VSME, when will it become an officially adopted standard, and—most importantly—what should out-of-scope SMEs do in the meantime?

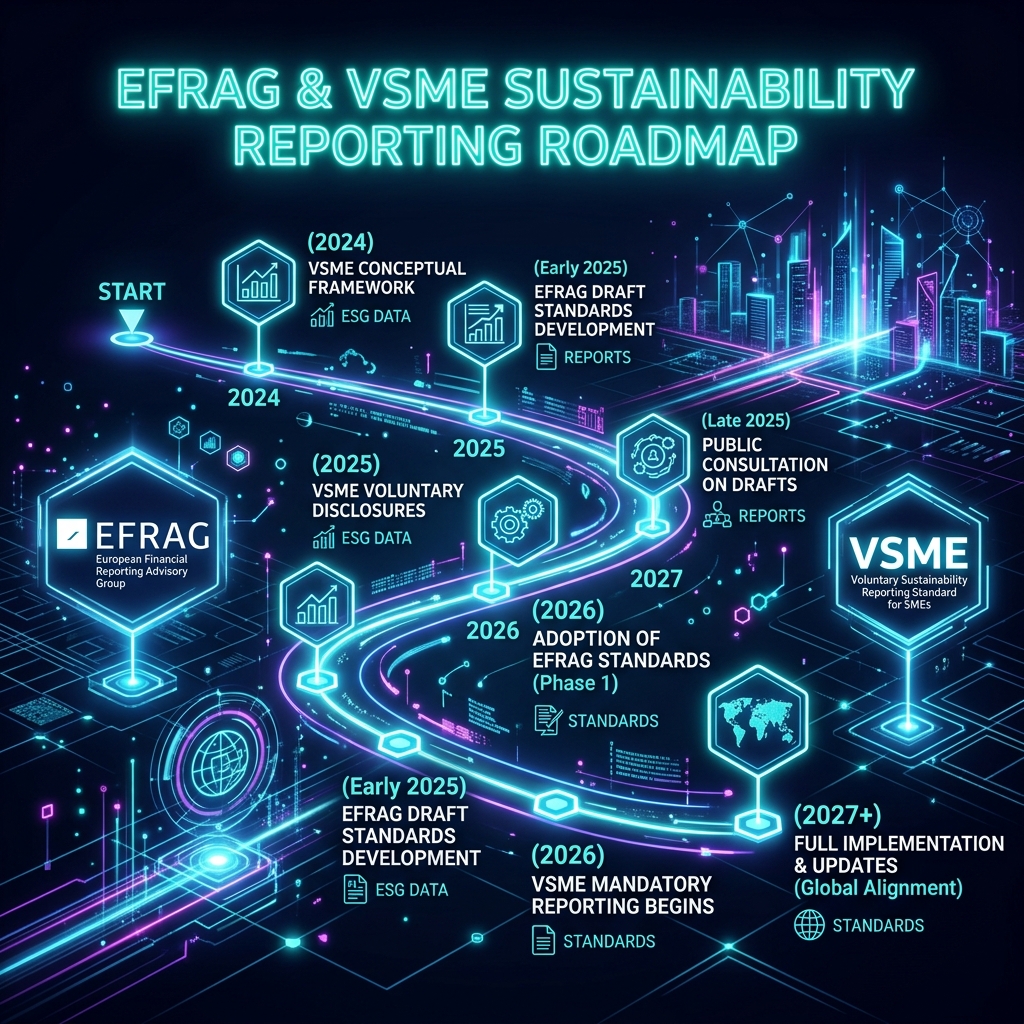

📅 VSME Post-Consultation Roadmap At-a-Glance

EFRAG processes public comments and categorizes technical recommendations regarding reporting complexity and audit rules.

EFRAG updates the disclosure text (B1–B11 basic disclosures) and solidifies the value chain cap guidelines.

The finalized electronic tagging schema is released, allowing software platforms to generate machine-readable VSME reports.

The European Commission formally adopts the VSME standard as a Delegated Act, establishing it as the statutory value chain cap.

1. The Post-Consultation Roadmap: Step-by-Step

The transition from a draft consultation to an officially adopted EU Delegated Act involves a structured process managed by EFRAG and the European Commission. Here is what the timeline looks like for the remainder of 2026 and early 2027.

Phase 1: Feedback Analysis (Summer 2026)

During this phase, EFRAG's technical secretariat compiles and reviews the hundreds of public responses submitted through the "Have Your Say" portal. The feedback is typically grouped into four main buckets:

- Feasibility & Complexity: Can micro-enterprises realistically compile these data points?

- Carbon Accounting (B3): Are the guidelines for Scope 1, 2, and 3 calculations clear enough?

- Supply Chain Pressures: Does the standard protect suppliers from excessive corporate requests?

- Digital Integration: How easily can software vendors integrate the standard's tagging schema?

Phase 2: Technical Drafting & Refinement (Fall 2026)

Following the feedback analysis, EFRAG's Sustainability Reporting Board (SRB) and Sustainability Reporting Technical Committee (SR TEG) will debate and draft adjustments. Key areas expected to undergo refinement include:

- The Value Chain Cap: Strengthening the legal ceiling introduced by the Omnibus I Directive to prevent large buyers from bypassing the VSME to ask for custom, non-standardized ESG data. (Read more in our analysis of ExecutESG's official consultation proposals).

- Simplified Disclosures: Streamlining the environmental (B3–B7) and social (B8–B10) disclosures to reduce reporting friction for companies with fewer than 50 employees.

Phase 3: Digital XBRL Taxonomy Publication (Late 2026)

One of the most important developments for the voluntary standard is its digitization. Alongside the text of the standard, EFRAG is developing an XBRL (eXtensible Business Reporting Language) taxonomy.

- Once finalized, this electronic taxonomy will allow software tools to tag data points automatically.

- SMEs will be able to export their reports as machine-readable files, which can be uploaded directly to public portals, bank systems, or customer databases without manual data entry.

Phase 4: Formal EU Adoption (Early 2027)

Once EFRAG delivers the finalized draft to the European Commission, the Commission will review it and initiate the adoption process. It is expected to be adopted as a Delegated Act in early 2027. Once adopted, it will serve as the official, unified EU reference point for all voluntary SME sustainability reporting.

2. Why the Core Disclosures of VSME Will Remain Stable

A common concern among small business owners is whether they should wait for the final version of the standard before starting their reporting process. The short answer is: No, you should not wait.

While technical wording and formatting will be refined during the post-consultation phase, the core structural skeleton of the VSME standard is already stable. EFRAG has built the voluntary standard on a modular architecture that has broad consensus:

- The Basic Module (B1–B11): Contains simple, qualitative, and quantitative disclosures (e.g., headcount, carbon emissions, collective bargaining). This serves as the entry-level baseline.

- The Narrative-Policies, Actions, and Targets (PAT) Module: Designed for companies that have formal sustainability policies in place.

- The Business Partners Module: Specifically structured to collect the precise data points that large corporate buyers require for their own CSRD reports.

Because this modular structure aligns directly with the underlying requirements of the Corporate Sustainability Reporting Directive (CSRD), the fundamental data points—especially Scope 1, 2, and 3 emissions—will not change. Any data you collect under the current draft will remain 100% relevant when the final standard goes live.

3. What SMEs Should Do in the Meantime

Waiting for early 2027 to begin sustainability reporting is a commercial risk. The pressure on SMEs is not driven by the European Commission; it is driven by the market:

Large Corporate Buyers Are Already in Scope

Large European enterprises must compile their first CSRD reports in 2025 (covering fiscal year 2024) and 2026. Because they are legally mandated to report their upstream supply chain emissions, they are already actively surveying their suppliers for carbon and ESG data. If you cannot provide this data, you risk losing your status as a preferred supplier.

Banks Are Linking Financing to ESG Data

Nordic and European financial institutions are rapidly integrating ESG risk assessments into their commercial lending processes. A completed, standardized VSME report gives your bank a credible, structured document to justify favorable lending rates.

The Rise of "Once-for-All" Reporting

The primary value of the EFRAG VSME framework is that it operates on the "once-for-all" principle. Instead of filling out 20 different custom Excel questionnaires from 20 different corporate customers, you compile a single VSME-compliant report and share it with everyone.

4. How to Get Started Today

If you want to protect your business from supply chain auditing fatigue and establish a competitive advantage in upcoming tenders, you can start today.

Step 1: Establish Your Reporting Boundary

Define which parts of your operations are included in your report. For most service and light manufacturing SMEs, this includes your main offices, operational facilities, and company vehicles.

Step 2: Calculate Your Energy & Carbon Baseline

Gather your electricity invoices, heating bills, and vehicle fuel logs. Under the EFRAG draft, calculating your Scope 1 and Scope 2 emissions is the core quantitative requirement of Disclosure B3.

Step 3: Use an Automated Wizard

You do not need to hire an expensive sustainability consultant or spend hours trying to understand regulatory jargon. Dedicated sustainability reporting software can guide you through the EFRAG guidelines step-by-step.

At ExecutESG, we believe that sustainability compliance should be accessible to every business. That is why our Basic Module is permanently free, allowing you to complete your first VSME report, calculate your carbon footprint automatically, and export your data as a clean PDF or Word document in under 15 minutes.

Create Your Free ExecutESG Account Today →

5. Frequently Asked Questions

Is voluntary CSRD reporting legally required for my SME? No. If your company is a non-listed SME (fewer than 250 employees, under €50m turnover, or under €25m balance sheet total), you are out of scope for mandatory CSRD reporting. VSME reporting is completely voluntary. However, your large corporate customers may require it as a contractual condition of business.

Will my current data collection become obsolete when the final VSME standard is adopted? No. The core data points of the VSME standard (employee counts, Scope 1 and 2 carbon calculations, gender pay gaps, and governance policies) are aligned with international standards (GHG Protocol and GRI) and will remain identical in the final standard.

What is the "Value Chain Cap"? The value chain cap is a legal rule introduced to protect SMEs. It prevents large CSRD-regulated enterprises from demanding more data from their SME suppliers than what is outlined in EFRAG's voluntary VSME standard. This prevents larger firms from pushing their administrative burden onto smaller partners.

How does the XBRL digital taxonomy help my business? The digital taxonomy acts like a barcode for sustainability data. When you use software like ExecutESG to generate your report, it exports a machine-readable digital file. Your customers and banks can import this file directly into their ESG software systems, eliminating manual data entry and proofreading.

This article was compiled by ExecutESG's regulatory compliance team. We update our guides regularly as EFRAG releases new technical clarifications and digital taxonomy updates.

Ready to compile your first audit-ready report? Create your free account on ExecutESG today →